Retirement provision is part of pay, not a side note. A role with no pension can still make sense, but only if you understand what the employer is actually offering, where the UK rules create exceptions, and how much of the package you would need to replace yourself. In this article I break down the practical impact on pay, the legal thresholds that matter in 2026, and the questions I would ask before I accepted the offer.

Why the missing pension changes both value and risk

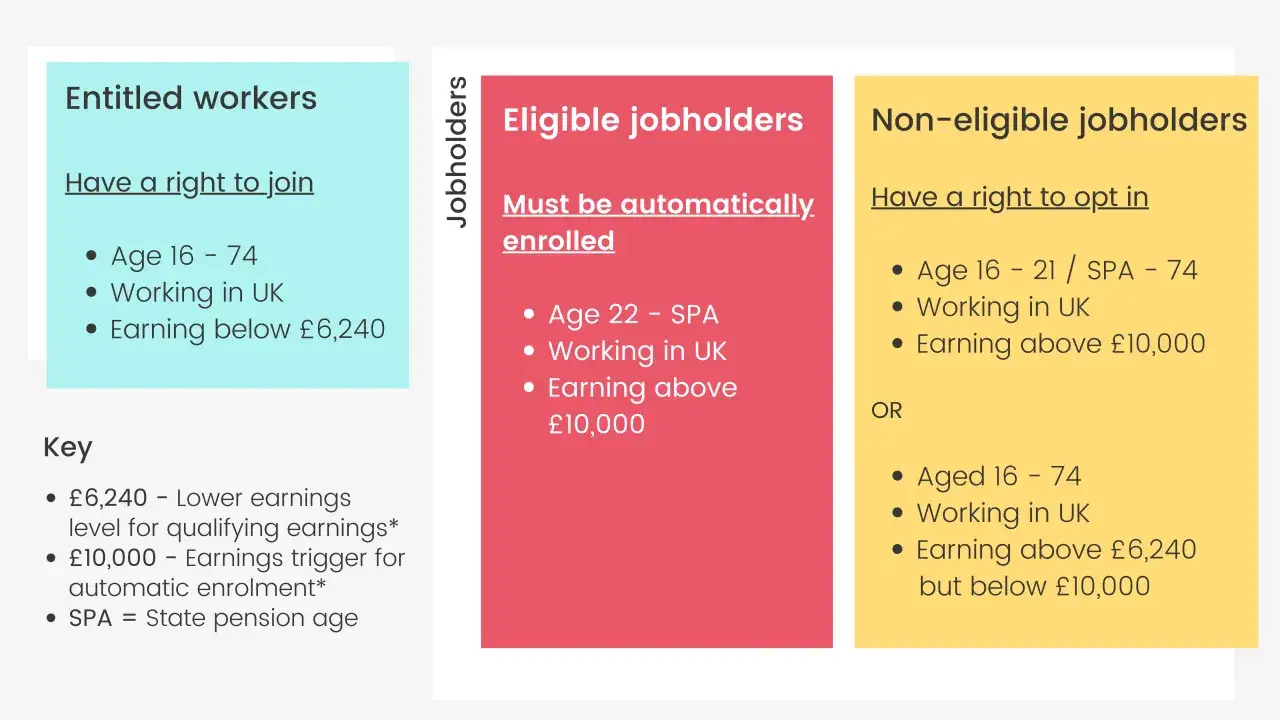

- In the UK, eligible workers are usually auto-enrolled if they are aged 22 to State Pension age and earn at least £10,000 a year.

- The minimum workplace pension contribution is 8% of qualifying earnings, with at least 3% paid by the employer.

- Not every absence means the employer is ignoring the rules, some workers can opt in or join under different conditions.

- The full new State Pension is £241.30 a week in 2026/27, but it is not enough to replace a normal salary.

- The real comparison is total reward, salary, pension, leave, sick pay, flexibility, and job security.

- If you take the role, set up your own retirement saving early and automate it.

What a missing pension really means in the UK

When I hear that a role has no pension, I first check whether the benefit is truly absent or whether the job simply falls outside automatic enrolment. The Pensions Regulator says UK employers must put certain staff into a workplace scheme and contribute to it, but the duty depends on age, earnings, and worker status.

- Eligible jobholder - usually aged 22 to State Pension age and earning above £10,000 a year. The employer must auto-enrol and contribute.

- Non-eligible jobholder - usually aged 16 to 21, or State Pension age to 74, or earning between £6,240 and £10,000. They can opt in, and the employer must then contribute.

- Entitled worker - usually earning below £6,240. They can join a scheme, but the employer does not have to contribute.

That distinction matters because a missing pension can mean a genuine benefit gap, or it can mean you are looking at a waiting period, a contract role, or the wrong employment status altogether. Once that is clear, the next question is simple: what is the gap worth in money terms?

Why the real cost is bigger than the headline salary

The missing pension is not just the employer’s contribution disappearing. It also changes how I compare offers, because I stop treating headline salary as the whole story and start looking at total reward.

| Annual salary | Qualifying earnings | Minimum employer contribution | Total minimum contribution |

|---|---|---|---|

| £30,000 | £23,760 | £712.80 | £1,900.80 |

| £45,000 | £38,760 | £1,162.80 | £3,100.80 |

These examples use the 2026/27 qualifying-earnings band of £6,240 to £50,270. In a different scheme, the calculation may use pensionable pay instead, so the exact figure can change, but the point does not: the lost value grows quickly as salary rises.

GOV.UK confirms the full new State Pension is £241.30 a week in 2026/27, which is about £12,547.60 a year. That is a base, not a replacement for a mid-career income, so a role without retirement saving shifts more risk onto you. Once the numbers are clear, the next step is to separate a legitimate exception from a warning sign.

When the absence is normal and when it is a warning sign

Not every role with no pension is badly designed. Some are simply outside the automatic-enrolment rules, while others are structured so that you can opt in later. I read the context before I judge the offer.

| Situation | What it usually means | What to check |

|---|---|---|

| Age 16 to 21, or at State Pension age and above | Not auto-enrolled yet, or no longer eligible for automatic enrolment | Can you opt in, and will the employer contribute? |

| Earning between £6,240 and £10,000 | Not auto-enrolled, but you can opt in | Ask for the employer contribution in writing |

| Earning below £6,240 | You can join, but the employer does not have to contribute | What alternative saving plan is realistic? |

| Self-employed or genuinely freelance | No employer scheme by default | Set up a personal pension or SIPP |

| Permanent employee with no pension mentioned | Could be an omission, a waiting period, or a compliance problem | Ask HR to confirm the arrangement and dates |

Some employers also use postponement for up to three months, often while probation runs or payroll is being set up. That is allowed, but they must tell you in writing and explain when automatic enrolment will be assessed.

If a role does not fit any of those buckets and still offers nothing, I treat that as a question for HR, not a footnote. That brings me to the questions I would ask before I signed anything.

What I would ask before I accepted the role

I would not let "we do not offer pension" end the conversation. I would ask for the structure in writing and test the package against comparable roles.

- Am I excluded because of age, earnings, contract type, or a waiting period?

- Is there a workplace scheme I can join, even if I am not auto-enrolled yet?

- If I can opt in, what employer contribution applies?

- Is the role being postponed for up to three months?

- Is there a cash allowance instead of a pension contribution?

- How does the total package compare with similar public sector posts?

If the job is agency, fixed-term, or project-based, I also ask whether the day rate already bakes in the cost of self-funded retirement saving. A salary that looks competitive on paper can become ordinary once pension, holiday, sick pay, and stability are priced properly.

That leads to the most practical part, how to cover the gap if you take the job anyway.

How to protect your retirement if the job does not include one

If I accept a role without workplace saving, I treat my own pension as a non-negotiable line item. The easiest version is a personal pension or SIPP with an automatic monthly transfer, because saving only works when it is boring and predictable.

- Start with at least the amount you would have expected the employer to pay under automatic enrolment, or as close to it as your budget allows.

- Use tax relief to reduce the net cost of the contribution, rather than waiting for a perfect month that never comes.

- Keep an emergency fund separate, so short-term pressure does not raid long-term saving.

- Review your contribution when pay changes, not just when you remember to.

- Check your National Insurance record and forecast so you know what the State Pension is likely to cover.

I also prefer to be explicit about trade-offs: if an employer offers a higher salary in place of a pension, I want to see that cash difference redirected into retirement saving before lifestyle spending takes over. That is the part most people mean well about and then delay.

For public sector careers, this discipline matters even more when the role is a bridge into a future permanent post with better benefits.

How I would judge a public sector offer over time

In a public sector move, I rarely judge the package on salary alone. I look at the pension position, annual leave, sick pay, progression, flexibility, training, and whether the role is stable enough to justify a short-term compromise.

- Does the salary offset the missing employer contribution?

- Is the contract short enough that the absence is manageable, or long enough that it becomes expensive?

- Are the other benefits strong enough to compensate, especially leave and sick pay?

- Will the role lead to a better-paid post with proper retirement provision?

- Can I replace the missing saving without making the budget unrealistic?

A package with no pension can still be fair if the numbers are explicit, the contract is deliberate, and you replace the missing saving on purpose. If any of those pieces is vague, I would treat the offer as incomplete until the employer can explain it properly in writing.